At a USC School of Law Commencement speech in May 2007, Charlie Munger, Warren Buffett’s right hand man at Berkshire Hathaway, tells a lovely story about the quantum physicist and Nobel Laureate Max Planck.

After winning the Nobel Prize for Physics in 1918, Planck toured around Germany giving a lecture about his specific field. The chauffeur who accompanied him on the tour heard the speech so often that he ended up committing it to memory. When they arrived in Munich, the chauffeur asked Planck if he could give the speech instead, since he knew it off by heart, while Planck acted as the chauffeur.

Planck agreed. After the speech, a member of the audience asked a particularly tough question. The chauffeur (as Planck) replied that he couldn’t believe that someone in such an advanced city as Munich could ask such an elementary question; as such, he would let his chauffeur (Planck himself) respond.

“In this world,” (says Munger) “we have two kinds of knowledge. One is Planck knowledge, the people who really know. They’ve paid the dues, they have the aptitude. And then we’ve got chauffeur knowledge. They have learned the talk. They may have a big head of hair, they may have fine temper in the voice, they’ll make a hell of an impression. But in the end, all they have is chauffeur knowledge.”

Our society tends to venerate true scientists, but we often overlook how difficult it can be for bold (and correct) new insights to be accepted by the establishment. As Planck himself said,

“A new scientific truth does not triumph by convincing its opponents and making them see the light, but rather because its opponents eventually die, and a new generation grows up that is familiar with it.”

This has been popularly paraphrased as,

“Science advances one funeral at a time.”

Economics, of course, is not a true science.

The philosopher Karl Popper identified the principle of falsifiability as an indicator of a properly scientific theory. A scientific hypothesis must be falsifiable – i.e. testable. For as long as rigorous testing affirms the theory, it is deemed to be valid. This validity is always conditional, however. Clearly, the moment it fails rigorous testing, the theory is shown to be no longer valid, and it must be replaced by some superior theory.

Sadly, in the realm of conventional (that is to say, Keynesian) economics, no such rigour applies. As Popper saw it, many branches of applied science, especially the social sciences, are not scientific in any real sense of the word because they offer no potential for falsification. Conventional economics is a classic example.

Meet the Austrians

But not all economic schools amount to pseudo science. The one that has been most influential for us and that has helped us navigate these extraordinary financial conditions – especially in the aftermath of the Global Financial Crisis – is the so-called Austrian School.

Unlike Keynesian economics, Austrian economics places individual human beings – not some sterile economic model – at the heart of the story. Ludwig von Mises, one of the founding fathers of the Austrian School, titled his magnum opus ‘Human Action’.

Austrian economists put a premium on sound money, small government, and the rights of the individual. They venerate the entrepreneur as the prime mover in the economy. Government tends to be the enemy. (See the counter-Covid insanity, climate change insanity and European energy policy for more on this theme.) But as Austrians see the world, any intervention by the state in the mutual cooperation of free individuals is neither reasonable nor just. And price fixing – in money, as in other commodities – is not just unwise but actively counterproductive. Yet the central control of interest rates is precisely that – price fixing – and our current crisis is its bitter harvest.

To the Keynesian, government is there to save the economy every time it gets into trouble. To the Austrian, however, government is invariably the cause of the problems in the first place, and government should be as small as possible, not least to limit the malign effects of its constant intervention in what could otherwise be free markets.

Mises, and the Austrian School, matter now more than ever before. We are living through a peculiarly fraught period in what Mises called the ‘Crisis of Interventionism’. While our central banks pile intervention upon intervention, driving interest rates and bond yields and debauched currency values all over the shop, it is increasingly clear that our reserves of private wealth are becoming exhausted and imperilled – by government action.

Interventionism kills off the permanent portfolio

In his September 1999 book ‘Fail-Safe Investing’, the libertarian Harry Browne (re)introduced the world to his “permanent portfolio”. This was a form of diversified investment that would cater to any economic or financial eventuality.

The essence of the “permanent portfolio” is simplicity. Browne advocated a portfolio split equally between four asset classes, namely:

- 25% in cash;

- 25% in long term US Treasury bonds;

- 25% in US stocks;

- 25% in gold.

The rationale behind each of these holdings was as follows:

- Cash, in the form of a money market fund, serves as a portfolio ‘hedge’ in times of tight money (rising interest rates) or recession.

- Bonds can be expected to do tolerably well in periods of prosperity, low inflation or deflation.

- Stocks, in the form of a low cost tracker fund, should provide strong returns during a period of prosperity.

- Gold, in the form of gold bullion coins, serves as a portfolio ‘hedge’ during periods of high inflation or heightened systemic distress.

And the “permanent portfolio” has delivered the goods – at least thus far.

In December 1982, a mutual fund managed roughly according to Harry Browne’s specifications was launched by the Permanent Portfolio Family of Funds, and you can see its annualised returns in the table below:

Source: http://www.lazyportfolioetf.com/allocation/harry-browne-permanent/

A 6.38% annualised return over the past 30 years stacks up pretty well for a portfolio that has only 25% of its assets allocated to the stock market and which also has a 25% holding in the form of cash.

But consider the headwinds that the “permanent portfolio” is now up against.

Fully half of the fund is held in the form of nominal assets that are not well placed to survive a high inflation environment.

Interest rates around the world, as we know, are now rising from their lowest levels in human history. This is not, as wilfully ignorant Keynesians would argue, the result of some kind of global savings glut, but rather as a deliberate policy of intervention on the part of the world’s central banks.

And as deposit rates have until very recently sunk to the floor and in some cases beneath it, they have dragged down the yields available on all forms of government bonds – helped, of course, by central bank purchases of those same bonds as part of coordinated QE programmes that Keynesians refuse to accept amount to massive market manipulation.

To put it another way, while the “permanent portfolio” has done an admirable job of capital preservation since it was established, it now faces insuperable challenges that the late Harry Browne could barely have dreamed would ever come about – even in his most lurid and fanciful nightmares.

The very idea that deposit interest rates could ever turn negative in a world of fiat money is offensive to rational thought.

Mainstream (i.e. Keynesian) economic theory has it that when interest rates are positive, by cutting them you stimulate the economy. This is straight out of every central banker’s crisis playbook: whenever you encounter a financial crisis or an economic shock, slash rates.

This has been the time-honoured response by central bankers since Alan Greenspan first cut rates in response to the (ultimately short-lived) crash of 1987.

But mainstream economic theory has nothing to say on the subject of what happens to participants in an economy when you force interest rates to zero and then below it.

Plausibly, below the so-called zero “lower bound”, behaviours change. Attitudes change. People become scared.

Keynesian economics requires that we all behave like homo economicus, a strictly rational agent focused purely on maximising our own economic utility (or profit).

The Austrians would posit something different. Below the zero “lower bound”, people become so terrified at the prospect of seeing their life savings eroded that they do something that the textbooks never envisaged: they start saving even more.

In a world below zero – our own financial world, until very recently – unintended consequences reign supreme.

Richard Koo, chief economist of the Nomura Research Institute, has written the definitive book about our current monetary predicament, ‘The Holy Grail of Macro-economics: Lessons from Japan’s Great Recession’.

As the first major developed economy to experience deflation, Japan has been a laboratory experiment for unorthodox monetary policy ever since.

Koo’s key point: in what he calls a “balance sheet recession” (i.e. a recession caused by a build-up of private sector debt rather than by the more traditional fluctuations of the (Keynesian) business cycle), people are more focused on deleveraging or saving than they are on spending or investing. To put it another way, people are more interested in survival than speculation.

Koo uses the analogy of a shopkeeper selling apples to describe Japan’s failed flirtation with QE back in 2001:

“The central bank’s implementation of QE at a time of zero interest rates was similar to a shopkeeper who, unable to sell more than 100 apples a day at $1 each, tries stocking the shelves with 1,000 apples, and when that has no effect, adds another 1,000. As long as the price remains the same, there is no reason consumer behaviour should change – sales will remain stuck at about 100 even if the shopkeeper puts 3,000 apples on display. This is essentially the story of QE, which not only failed to bring about economic recovery, but also failed to stop asset prices from falling well into 2003.”

Weird things happen below the “lower bound”. As savers get smaller and smaller returns on their capital, some of them choose to save even more. That is, of course, entirely logical – if not necessarily consistent with half-baked economic theory.

And if people are determined to save, there is damn all you can do to force them to spend – especially if they harbour fears for their future.

The great insight of the Austrian School is that the economy cannot be reduced to a simple model, and if you try, you will end up with a grossly imperfect model. The economy consists of the interactions of over 7 billion people. The economy is us. It is far too complicated to be reduced to some overly simplified “cause and effect” statements about monetary policy. If today’s economists were serious about reforming their pseudo science, they could start with abandoning abstract mathematical theory, and taking some lessons in psychology and history.

There are many things about the modern economic world that we cannot control. Derisory interest rates and mostly overpriced financial assets are among them.

But one thing we can control is how our portfolios are positioned. William Bernstein in ‘The Intelligent Asset Allocator’ rightly observed:

“Asset allocation is the only factor affecting your investments that you can actually influence.”

So if we were tasked with coming up with an alternative “permanent portfolio” for our times, what might it look like ?

In the cause of capital preservation (first and foremost) and then prudent capital growth, our asset allocation model would look like the one below:

The permanent portfolio – financial repression version

Please note, this is not a criticism of the “permanent portfolio” or of Harry Browne’s original intentions. Rather, this is a proposed refinement of that portfolio that takes into account the extraordinary market distortions that the world’s central banks have caused in their decades-long fight against deflation.

Given that the Austrians regard value as inherently subjective, we don’t pretend to have a “one size fits all solution” – investors requiring income will naturally migrate to bonds and stocks, for example, but may feel uncomfortable holding trend-following funds and gold, because they don’t distribute any income; their returns come purely from changes in price.

Unconstrained value equities form the first component of the portfolio (see last week’s commentary for precisely what we look for). Markets have clearly been artificially suppressed and controlled for years but, in a battle royale between governments and markets, we expect the markets ultimately to win out. And in the context of the world’s major tradeable asset classes, a subset of the listed equities universe that focuses entirely on defensive valuations, a “margin of safety” and high quality is surely an acceptable compromise.

By uncorrelated funds we mean specifically systematic trend-following funds. Systematic trend-following funds or CTAs (Commodity Trading Advisers), also known as managed futures funds, have historically been a great hedge against financial market instability.

And last, and by no means least, real assets – notably, the monetary metals, gold and silver. Why ? Because in a world where central banks know no limits when it comes to money printing or experiments in debauching the purchasing power of unbacked fiat money, it makes sense to own a type of money that simply can’t be printed on demand at the whim of an unelected monetary technocrat. Gold and silver fulfil that requirement. It helps the investment thesis today that mining companies happen to comprise the cheapest sector within the stock market.

Note that the ‘nominal’ asset exposure of this portfolio model is absolutely minimal. This is entirely intentional.

The great Austrian economist Ludwig von Mises had first-hand experience of the Weimer hyperinflation of 1923. He knew what happened to a financial system in which credit creation spiralled out of control.

This is what Mises had to say about the terminal stages of a great inflationary experiment. Central bank stimulus can go on for some time, with seemingly benign, or at least not traumatic, results.

“But then finally the masses wake up. They become suddenly aware of the fact that inflation is a deliberate policy and will go on endlessly. A breakdown occurs. The crack-up boom appears. Everybody is anxious to swap his money against ‘real’ goods, no matter whether he needs them or not, no matter how much money he has to pay for them. Within a very short time, within a few weeks or even days, the things which were used as money are no longer used as media of exchange. They become scrap paper. Nobody wants to give away anything against it.

“It was this that happened with the Continental currency in America in 1781, with the French Mandats territoriaux [paper bank notes issued as currency by the French Directory in 1796 to replace the Assignats which had become virtually worthless] and with the German mark in 1923. It will happen again whenever the same conditions appear, this time with the dollar and euro, with all paper currencies at once. If money has to be used as a medium of exchange, public opinion must not believe that the quantity of this thing will increase beyond all bounds. Inflation is a policy that cannot last.”

It is our contention that Mises’ “crack-up boom” may have already begun. It is not yet recognised as such by mainstream economists because a) mainstream economists are idiots, and b) financial asset prices do not feature in conventional measures of inflation such as the CPI. But we would argue that the rush into real assets has already started. (It recently emerged that the Bank for International Settlements, the so-called central bank’s central bank, has just bought 500 tonnes of gold. They were unlikely doing so for aesthetic reasons.)

Mises also warned about the final stages of a credit boom:

“There is no means of avoiding a final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as a result of a voluntary abandonment of further credit expansion or later as a final and total catastrophe of the currency system involved.”

Since our monetary leaders have made it abundantly clear that the “voluntary abandonment of further credit expansion” is not on the cards, and if Mises is right, then the answer is clear: do not leave a meaningful part of your portfolio exposed to the risk inherent in the ownership of paper money. And do retain exposure to the monetary metals, gold and silver.

We give the last word this week to Alasdair Macleod, a 40 year City veteran who is now the Head of Research at Goldmoney. His years of experience in financial services have convinced Alasdair that unsound monetary policies are the most destructive weapon that governments can use against the common man. Accordingly, his mission is now to educate and inform the public in layman’s terms what governments do with money and how to protect themselves from the consequences. The following extract is taken from a speech given to the Committee for Monetary Research and Education in New York on 20 October 2011:

“I support sound money for two very good reasons. Firstly, it is a basic human right to choose to save, without our savings being debased by the tax of monetary inflation. Those who are worst affected by this inflation tax are not the rich, they benefit; but the poor and the barely well-off, which is why monetary inflation undermines society and why the right to sound money should be respected. If government gives itself a monopoly over money, it has a duty to protect the property rights vested in it. Secondly, it is a basic right for us to own our own money rather than have it owned by the banks. For them to take our money and expand credit on the back of it debases it. It is an abuse of an individual’s property rights and a banking licence is a government licence to do so. If anyone else was to do this, they would be guilty of fraud. Banks should be custodians of our money, and it should not appear in their balance sheets as their property.

“Sound money guarantees a stable yet progressive economy where people are truly equal. It allows people to save properly for their retirement so that they will not become a burden on the state. It leads to democracy voting for small governments. It encourages peaceful trade and discourages war. It is the only path, after this mess, that leads us to long-lasting and peaceful prosperity. We really need everyone to understand this for the sake of our future.”

………….

As you may know, we also manage bespoke investment portfolios for private clients internationally. We would be delighted to help you, too. Because of the current heightened market volatility we are offering a completely free financial review, with no strings attached, to see if our value-oriented approach might benefit your portfolio -with no obligation at all:

Get your Free

financial review

Tim Price is co-manager of the VT Price Value Portfolio and author of ‘Investing through the Looking Glass: a rational guide to irrational financial markets’. You can access a full archive of these weekly investment commentaries here. You can listen to our regular ‘State of the Markets’ podcasts, with Paul Rodriguez of ThinkTrading.com, here. Email us: info@pricevaluepartners.com

Price Value Partners manage investment portfolios for private clients. We also manage the VT Price Value Portfolio, an unconstrained global fund investing in Benjamin Graham-style value stocks and specialist managed funds.

At a USC School of Law Commencement speech in May 2007, Charlie Munger, Warren Buffett’s right hand man at Berkshire Hathaway, tells a lovely story about the quantum physicist and Nobel Laureate Max Planck.

After winning the Nobel Prize for Physics in 1918, Planck toured around Germany giving a lecture about his specific field. The chauffeur who accompanied him on the tour heard the speech so often that he ended up committing it to memory. When they arrived in Munich, the chauffeur asked Planck if he could give the speech instead, since he knew it off by heart, while Planck acted as the chauffeur.

Planck agreed. After the speech, a member of the audience asked a particularly tough question. The chauffeur (as Planck) replied that he couldn’t believe that someone in such an advanced city as Munich could ask such an elementary question; as such, he would let his chauffeur (Planck himself) respond.

“In this world,” (says Munger) “we have two kinds of knowledge. One is Planck knowledge, the people who really know. They’ve paid the dues, they have the aptitude. And then we’ve got chauffeur knowledge. They have learned the talk. They may have a big head of hair, they may have fine temper in the voice, they’ll make a hell of an impression. But in the end, all they have is chauffeur knowledge.”

Our society tends to venerate true scientists, but we often overlook how difficult it can be for bold (and correct) new insights to be accepted by the establishment. As Planck himself said,

“A new scientific truth does not triumph by convincing its opponents and making them see the light, but rather because its opponents eventually die, and a new generation grows up that is familiar with it.”

This has been popularly paraphrased as,

“Science advances one funeral at a time.”

Economics, of course, is not a true science.

The philosopher Karl Popper identified the principle of falsifiability as an indicator of a properly scientific theory. A scientific hypothesis must be falsifiable – i.e. testable. For as long as rigorous testing affirms the theory, it is deemed to be valid. This validity is always conditional, however. Clearly, the moment it fails rigorous testing, the theory is shown to be no longer valid, and it must be replaced by some superior theory.

Sadly, in the realm of conventional (that is to say, Keynesian) economics, no such rigour applies. As Popper saw it, many branches of applied science, especially the social sciences, are not scientific in any real sense of the word because they offer no potential for falsification. Conventional economics is a classic example.

Meet the Austrians

But not all economic schools amount to pseudo science. The one that has been most influential for us and that has helped us navigate these extraordinary financial conditions – especially in the aftermath of the Global Financial Crisis – is the so-called Austrian School.

Unlike Keynesian economics, Austrian economics places individual human beings – not some sterile economic model – at the heart of the story. Ludwig von Mises, one of the founding fathers of the Austrian School, titled his magnum opus ‘Human Action’.

Austrian economists put a premium on sound money, small government, and the rights of the individual. They venerate the entrepreneur as the prime mover in the economy. Government tends to be the enemy. (See the counter-Covid insanity, climate change insanity and European energy policy for more on this theme.) But as Austrians see the world, any intervention by the state in the mutual cooperation of free individuals is neither reasonable nor just. And price fixing – in money, as in other commodities – is not just unwise but actively counterproductive. Yet the central control of interest rates is precisely that – price fixing – and our current crisis is its bitter harvest.

To the Keynesian, government is there to save the economy every time it gets into trouble. To the Austrian, however, government is invariably the cause of the problems in the first place, and government should be as small as possible, not least to limit the malign effects of its constant intervention in what could otherwise be free markets.

Mises, and the Austrian School, matter now more than ever before. We are living through a peculiarly fraught period in what Mises called the ‘Crisis of Interventionism’. While our central banks pile intervention upon intervention, driving interest rates and bond yields and debauched currency values all over the shop, it is increasingly clear that our reserves of private wealth are becoming exhausted and imperilled – by government action.

Interventionism kills off the permanent portfolio

In his September 1999 book ‘Fail-Safe Investing’, the libertarian Harry Browne (re)introduced the world to his “permanent portfolio”. This was a form of diversified investment that would cater to any economic or financial eventuality.

The essence of the “permanent portfolio” is simplicity. Browne advocated a portfolio split equally between four asset classes, namely:

The rationale behind each of these holdings was as follows:

And the “permanent portfolio” has delivered the goods – at least thus far.

In December 1982, a mutual fund managed roughly according to Harry Browne’s specifications was launched by the Permanent Portfolio Family of Funds, and you can see its annualised returns in the table below:

Source: http://www.lazyportfolioetf.com/allocation/harry-browne-permanent/

A 6.38% annualised return over the past 30 years stacks up pretty well for a portfolio that has only 25% of its assets allocated to the stock market and which also has a 25% holding in the form of cash.

But consider the headwinds that the “permanent portfolio” is now up against.

Fully half of the fund is held in the form of nominal assets that are not well placed to survive a high inflation environment.

Interest rates around the world, as we know, are now rising from their lowest levels in human history. This is not, as wilfully ignorant Keynesians would argue, the result of some kind of global savings glut, but rather as a deliberate policy of intervention on the part of the world’s central banks.

And as deposit rates have until very recently sunk to the floor and in some cases beneath it, they have dragged down the yields available on all forms of government bonds – helped, of course, by central bank purchases of those same bonds as part of coordinated QE programmes that Keynesians refuse to accept amount to massive market manipulation.

To put it another way, while the “permanent portfolio” has done an admirable job of capital preservation since it was established, it now faces insuperable challenges that the late Harry Browne could barely have dreamed would ever come about – even in his most lurid and fanciful nightmares.

The very idea that deposit interest rates could ever turn negative in a world of fiat money is offensive to rational thought.

Mainstream (i.e. Keynesian) economic theory has it that when interest rates are positive, by cutting them you stimulate the economy. This is straight out of every central banker’s crisis playbook: whenever you encounter a financial crisis or an economic shock, slash rates.

This has been the time-honoured response by central bankers since Alan Greenspan first cut rates in response to the (ultimately short-lived) crash of 1987.

But mainstream economic theory has nothing to say on the subject of what happens to participants in an economy when you force interest rates to zero and then below it.

Plausibly, below the so-called zero “lower bound”, behaviours change. Attitudes change. People become scared.

Keynesian economics requires that we all behave like homo economicus, a strictly rational agent focused purely on maximising our own economic utility (or profit).

The Austrians would posit something different. Below the zero “lower bound”, people become so terrified at the prospect of seeing their life savings eroded that they do something that the textbooks never envisaged: they start saving even more.

In a world below zero – our own financial world, until very recently – unintended consequences reign supreme.

Richard Koo, chief economist of the Nomura Research Institute, has written the definitive book about our current monetary predicament, ‘The Holy Grail of Macro-economics: Lessons from Japan’s Great Recession’.

As the first major developed economy to experience deflation, Japan has been a laboratory experiment for unorthodox monetary policy ever since.

Koo’s key point: in what he calls a “balance sheet recession” (i.e. a recession caused by a build-up of private sector debt rather than by the more traditional fluctuations of the (Keynesian) business cycle), people are more focused on deleveraging or saving than they are on spending or investing. To put it another way, people are more interested in survival than speculation.

Koo uses the analogy of a shopkeeper selling apples to describe Japan’s failed flirtation with QE back in 2001:

“The central bank’s implementation of QE at a time of zero interest rates was similar to a shopkeeper who, unable to sell more than 100 apples a day at $1 each, tries stocking the shelves with 1,000 apples, and when that has no effect, adds another 1,000. As long as the price remains the same, there is no reason consumer behaviour should change – sales will remain stuck at about 100 even if the shopkeeper puts 3,000 apples on display. This is essentially the story of QE, which not only failed to bring about economic recovery, but also failed to stop asset prices from falling well into 2003.”

Weird things happen below the “lower bound”. As savers get smaller and smaller returns on their capital, some of them choose to save even more. That is, of course, entirely logical – if not necessarily consistent with half-baked economic theory.

And if people are determined to save, there is damn all you can do to force them to spend – especially if they harbour fears for their future.

The great insight of the Austrian School is that the economy cannot be reduced to a simple model, and if you try, you will end up with a grossly imperfect model. The economy consists of the interactions of over 7 billion people. The economy is us. It is far too complicated to be reduced to some overly simplified “cause and effect” statements about monetary policy. If today’s economists were serious about reforming their pseudo science, they could start with abandoning abstract mathematical theory, and taking some lessons in psychology and history.

There are many things about the modern economic world that we cannot control. Derisory interest rates and mostly overpriced financial assets are among them.

But one thing we can control is how our portfolios are positioned. William Bernstein in ‘The Intelligent Asset Allocator’ rightly observed:

“Asset allocation is the only factor affecting your investments that you can actually influence.”

So if we were tasked with coming up with an alternative “permanent portfolio” for our times, what might it look like ?

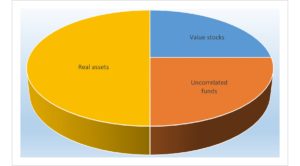

In the cause of capital preservation (first and foremost) and then prudent capital growth, our asset allocation model would look like the one below:

The permanent portfolio – financial repression version

Please note, this is not a criticism of the “permanent portfolio” or of Harry Browne’s original intentions. Rather, this is a proposed refinement of that portfolio that takes into account the extraordinary market distortions that the world’s central banks have caused in their decades-long fight against deflation.

Given that the Austrians regard value as inherently subjective, we don’t pretend to have a “one size fits all solution” – investors requiring income will naturally migrate to bonds and stocks, for example, but may feel uncomfortable holding trend-following funds and gold, because they don’t distribute any income; their returns come purely from changes in price.

Unconstrained value equities form the first component of the portfolio (see last week’s commentary for precisely what we look for). Markets have clearly been artificially suppressed and controlled for years but, in a battle royale between governments and markets, we expect the markets ultimately to win out. And in the context of the world’s major tradeable asset classes, a subset of the listed equities universe that focuses entirely on defensive valuations, a “margin of safety” and high quality is surely an acceptable compromise.

By uncorrelated funds we mean specifically systematic trend-following funds. Systematic trend-following funds or CTAs (Commodity Trading Advisers), also known as managed futures funds, have historically been a great hedge against financial market instability.

And last, and by no means least, real assets – notably, the monetary metals, gold and silver. Why ? Because in a world where central banks know no limits when it comes to money printing or experiments in debauching the purchasing power of unbacked fiat money, it makes sense to own a type of money that simply can’t be printed on demand at the whim of an unelected monetary technocrat. Gold and silver fulfil that requirement. It helps the investment thesis today that mining companies happen to comprise the cheapest sector within the stock market.

Note that the ‘nominal’ asset exposure of this portfolio model is absolutely minimal. This is entirely intentional.

The great Austrian economist Ludwig von Mises had first-hand experience of the Weimer hyperinflation of 1923. He knew what happened to a financial system in which credit creation spiralled out of control.

This is what Mises had to say about the terminal stages of a great inflationary experiment. Central bank stimulus can go on for some time, with seemingly benign, or at least not traumatic, results.

“But then finally the masses wake up. They become suddenly aware of the fact that inflation is a deliberate policy and will go on endlessly. A breakdown occurs. The crack-up boom appears. Everybody is anxious to swap his money against ‘real’ goods, no matter whether he needs them or not, no matter how much money he has to pay for them. Within a very short time, within a few weeks or even days, the things which were used as money are no longer used as media of exchange. They become scrap paper. Nobody wants to give away anything against it.

“It was this that happened with the Continental currency in America in 1781, with the French Mandats territoriaux [paper bank notes issued as currency by the French Directory in 1796 to replace the Assignats which had become virtually worthless] and with the German mark in 1923. It will happen again whenever the same conditions appear, this time with the dollar and euro, with all paper currencies at once. If money has to be used as a medium of exchange, public opinion must not believe that the quantity of this thing will increase beyond all bounds. Inflation is a policy that cannot last.”

It is our contention that Mises’ “crack-up boom” may have already begun. It is not yet recognised as such by mainstream economists because a) mainstream economists are idiots, and b) financial asset prices do not feature in conventional measures of inflation such as the CPI. But we would argue that the rush into real assets has already started. (It recently emerged that the Bank for International Settlements, the so-called central bank’s central bank, has just bought 500 tonnes of gold. They were unlikely doing so for aesthetic reasons.)

Mises also warned about the final stages of a credit boom:

“There is no means of avoiding a final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as a result of a voluntary abandonment of further credit expansion or later as a final and total catastrophe of the currency system involved.”

Since our monetary leaders have made it abundantly clear that the “voluntary abandonment of further credit expansion” is not on the cards, and if Mises is right, then the answer is clear: do not leave a meaningful part of your portfolio exposed to the risk inherent in the ownership of paper money. And do retain exposure to the monetary metals, gold and silver.

We give the last word this week to Alasdair Macleod, a 40 year City veteran who is now the Head of Research at Goldmoney. His years of experience in financial services have convinced Alasdair that unsound monetary policies are the most destructive weapon that governments can use against the common man. Accordingly, his mission is now to educate and inform the public in layman’s terms what governments do with money and how to protect themselves from the consequences. The following extract is taken from a speech given to the Committee for Monetary Research and Education in New York on 20 October 2011:

“I support sound money for two very good reasons. Firstly, it is a basic human right to choose to save, without our savings being debased by the tax of monetary inflation. Those who are worst affected by this inflation tax are not the rich, they benefit; but the poor and the barely well-off, which is why monetary inflation undermines society and why the right to sound money should be respected. If government gives itself a monopoly over money, it has a duty to protect the property rights vested in it. Secondly, it is a basic right for us to own our own money rather than have it owned by the banks. For them to take our money and expand credit on the back of it debases it. It is an abuse of an individual’s property rights and a banking licence is a government licence to do so. If anyone else was to do this, they would be guilty of fraud. Banks should be custodians of our money, and it should not appear in their balance sheets as their property.

“Sound money guarantees a stable yet progressive economy where people are truly equal. It allows people to save properly for their retirement so that they will not become a burden on the state. It leads to democracy voting for small governments. It encourages peaceful trade and discourages war. It is the only path, after this mess, that leads us to long-lasting and peaceful prosperity. We really need everyone to understand this for the sake of our future.”

………….

As you may know, we also manage bespoke investment portfolios for private clients internationally. We would be delighted to help you, too. Because of the current heightened market volatility we are offering a completely free financial review, with no strings attached, to see if our value-oriented approach might benefit your portfolio -with no obligation at all:

Get your Free

financial review

Tim Price is co-manager of the VT Price Value Portfolio and author of ‘Investing through the Looking Glass: a rational guide to irrational financial markets’. You can access a full archive of these weekly investment commentaries here. You can listen to our regular ‘State of the Markets’ podcasts, with Paul Rodriguez of ThinkTrading.com, here. Email us: info@pricevaluepartners.com

Price Value Partners manage investment portfolios for private clients. We also manage the VT Price Value Portfolio, an unconstrained global fund investing in Benjamin Graham-style value stocks and specialist managed funds.

Take a closer look

Take a look at the data of our investments and see what makes us different.

LOOK CLOSERSubscribe

Sign up for the latest news on investments and market insights.

KEEP IN TOUCHContact us

In order to find out more about PVP please get in touch with our team.

CONTACT USTim Price